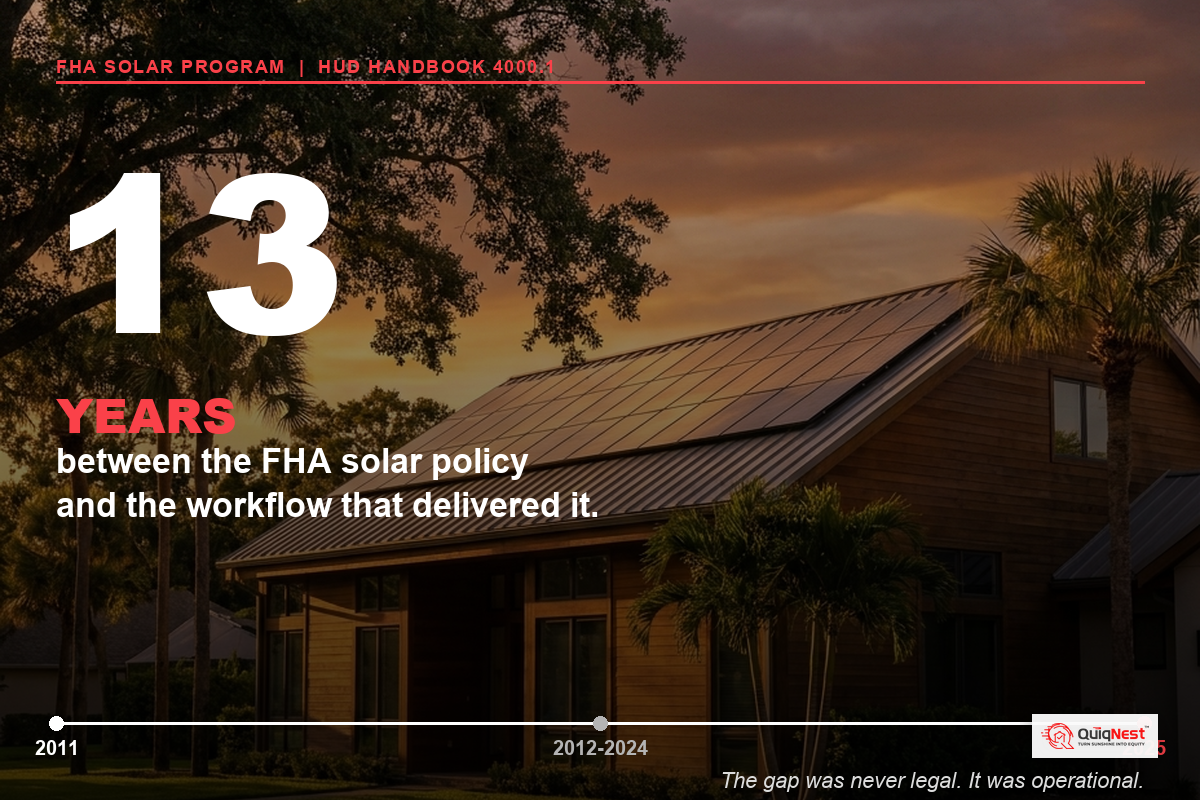

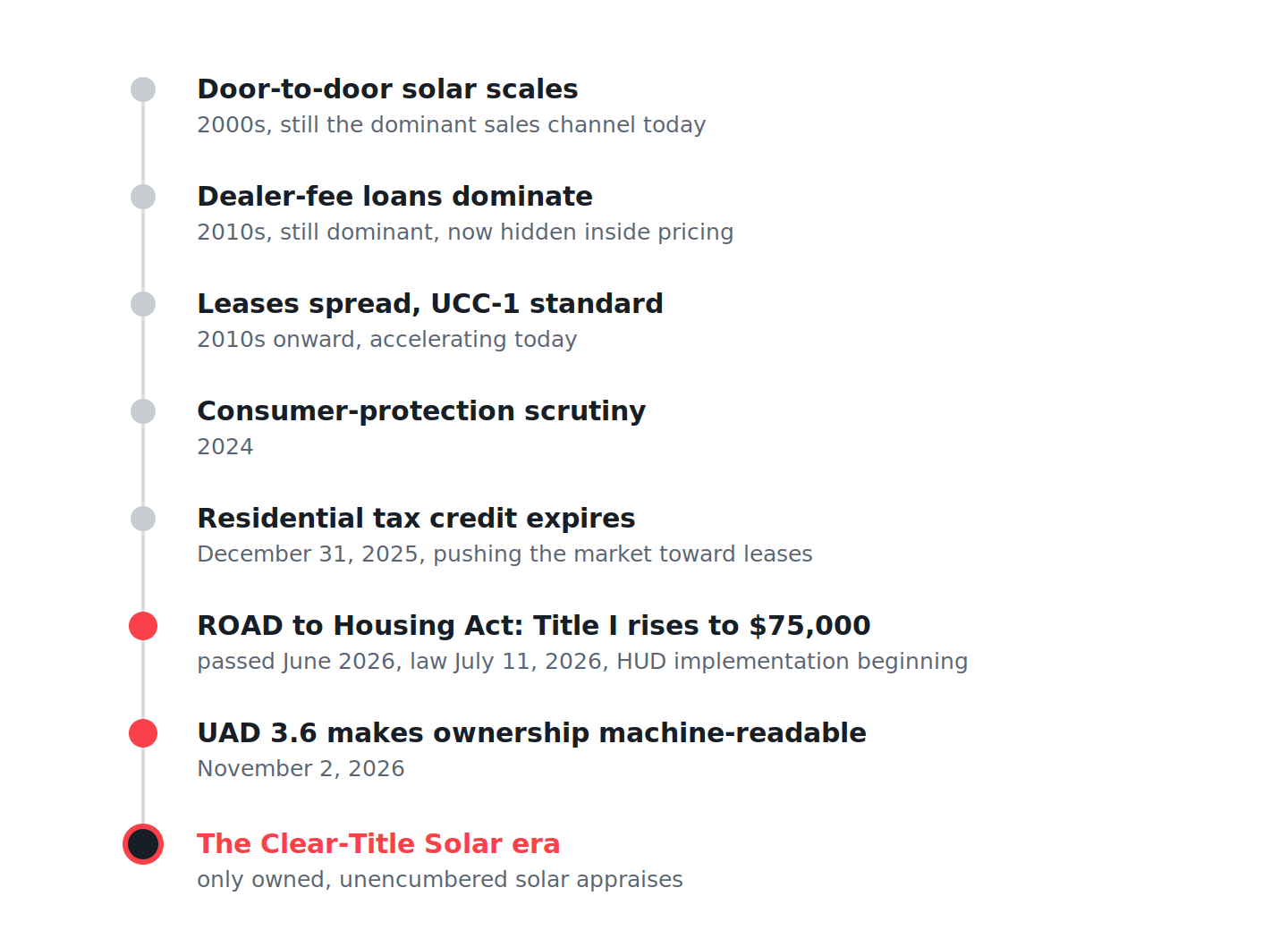

Something unusual happened in Washington this week. Congress passed the 21st Century ROAD Act in June, and on July 10, 2026, it became law without the President's signature: neither signed nor vetoed, it simply crossed the constitutional finish line on its own. Laws that survive that way tell you something. Nobody was willing to stop this one.

Buried inside it is a change that matters enormously for homeowners thinking about solar: the FHA Title I home-improvement program, a federal lending pathway that has existed for decades, had its single-family ceiling raised from $25,000 to $75,000, with maximum terms extending from 20 years to as long as 30 years, at HUD's discretion, with HUD implementation now beginning. At the old $25,000 limit, the program could not cover a complete solar project. At $75,000, it can, with room to spare.

Why this matters more than it sounds

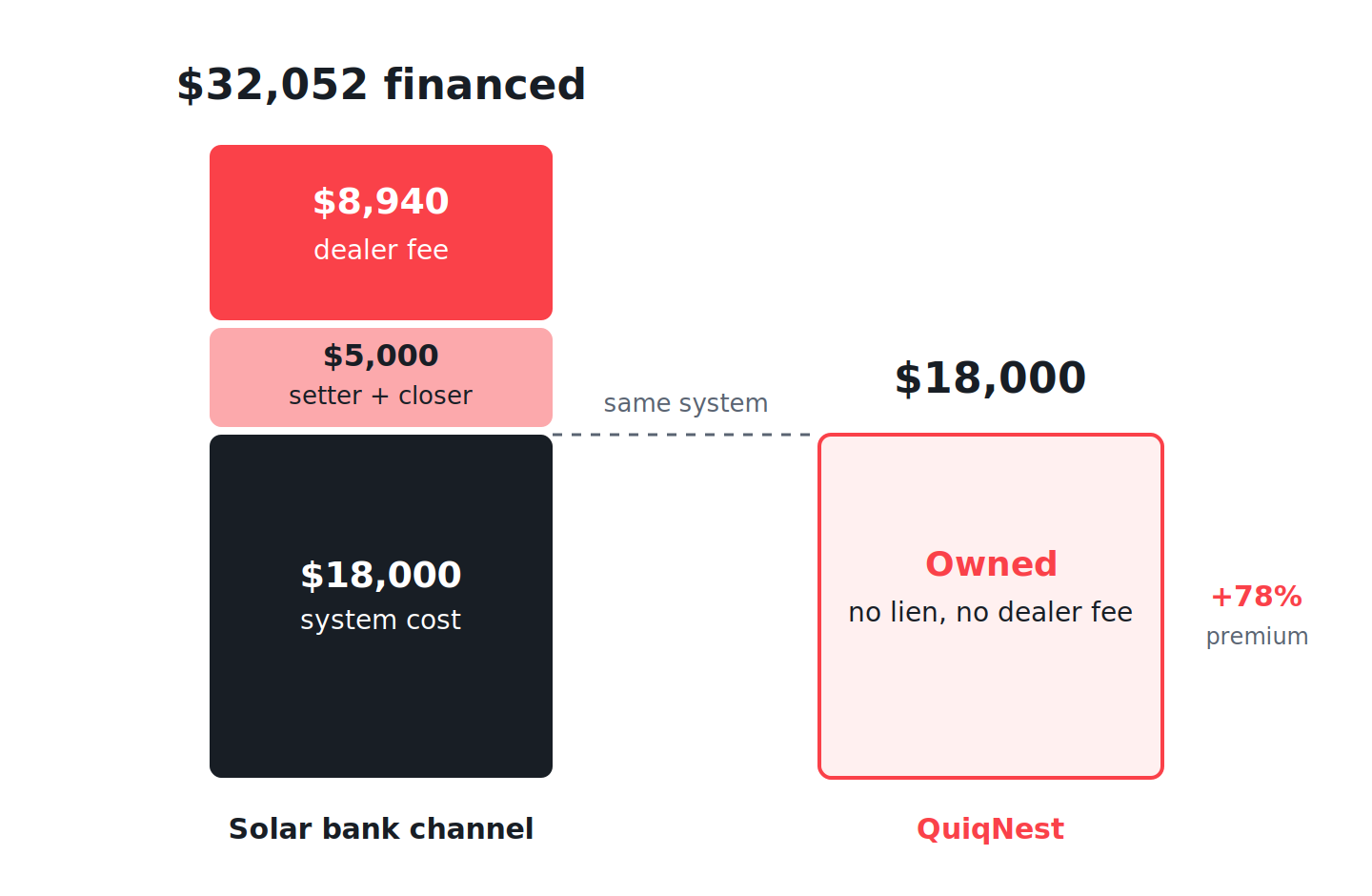

To understand why this is a big deal, you have to understand how most solar reaches homeowners today. It arrives through a sales machine: a knock on the door, a setter, a closer, and a financing structure with a dealer fee folded invisibly into the price. We have seen a solar bank's own internal calculator turn an $18,000 system into a $32,052 financed amount. The alternative most companies offer is a lease, where you never own the system at all, yet a lien still gets filed against your home.

Both structures share the same fatal flaw: they cannot become home equity. A homeowner who owes $32,000 on an $18,000 system can never roll that solar into their mortgage, because no appraisal can support the payoff. A homeowner with a lease owns nothing to roll in. Either way, the door to the cleanest financial outcome, solar as part of your home rather than beside it, closes on the day of signing.

The bridge with a designed exit

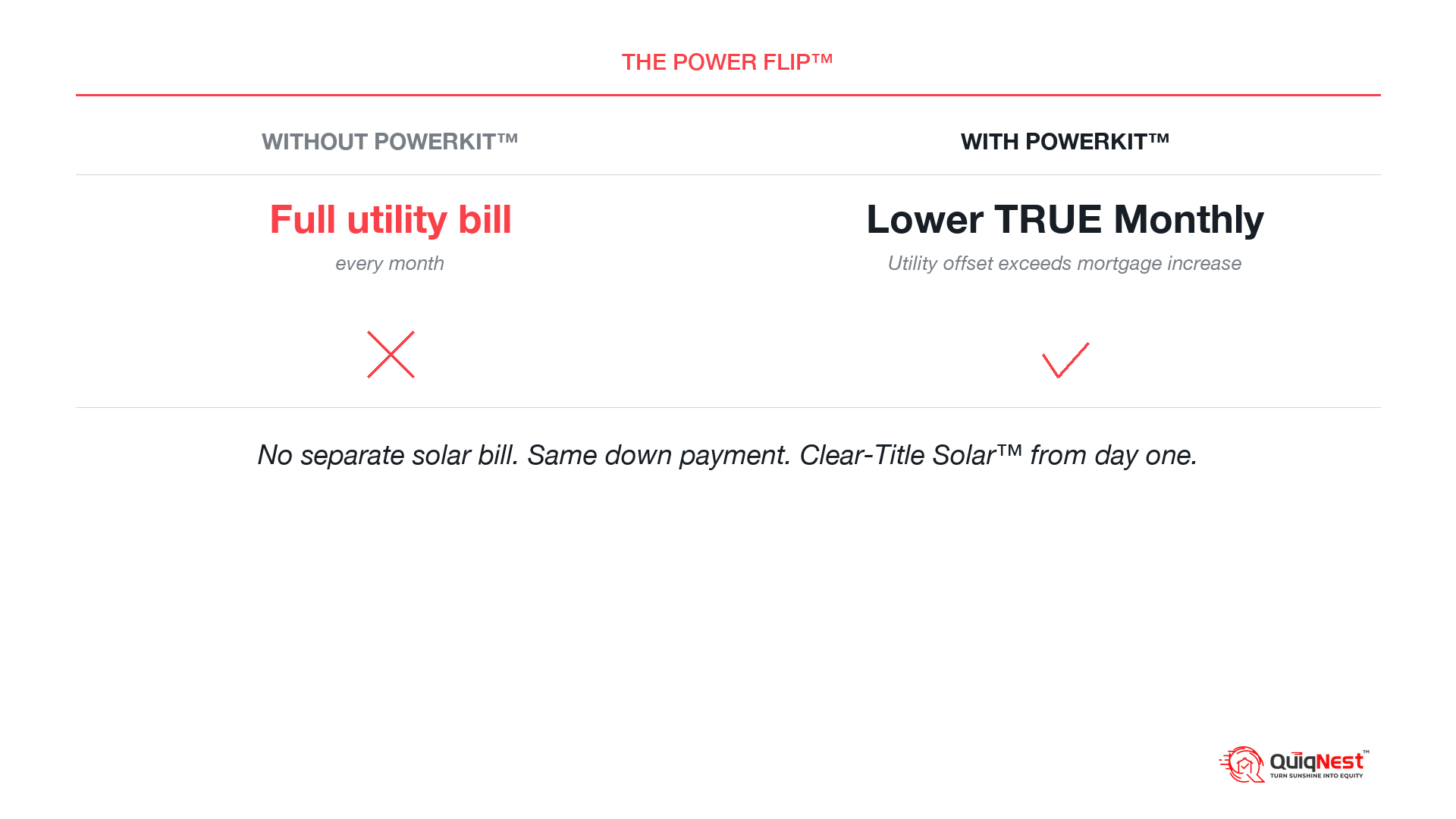

This is exactly the problem QuiqBridge™ was built to solve, and the ROAD Act just gave it a bigger rail to run on. QuiqBridge delivers owned solar at honest cost: no dealer fee in the price, no lease, no equipment lien on your home. It is a second payment, and we say that openly, but it is a second payment with a designed exit. Because the loan balance matches what the system honestly costs, the solar can consolidate into your primary mortgage through QuiqRefi™ when the timing is right, and the second payment disappears. One home, one payment, owned solar built into your equity. That is Clear-Title Solar™.

The clock behind the clock

There is a second date every homeowner considering solar should know: November 2, 2026. That is when the UAD 3.6 appraisal mandate takes effect, converting a solar system's ownership status into a structured, machine-readable field on every appraisal in the country. Owned, leased, or lien-encumbered: the appraisal will say which, automatically. Leased and encumbered systems are locked to zero contributory value. Only owned, unencumbered solar, the Clear-Title Solar™ standard, is positioned to hold value in your home's appraisal.

Put the two dates together and the picture is clear. The ROAD Act opens the door to financing owned solar the right way, and UAD 3.6 closes the door on pretending the other structures were ever equivalent.

What to do with this

If you already own your home and your power bill keeps climbing, the expanded pathway means owned, Clear-Title Solar™ is closer than it has ever been, without a door-to-door contract and without a lien. If you are shopping for a home, a Solar-Ready Home evaluated before you buy lets you build solar into your financing from day one. Either way, the question to ask about any solar offer is the one this whole story turns on: when this is done, who owns the system, and what does my title say?

See your QuiqBridge™ path at quiqnest.com/quiqbridge, or model your real monthly cost with Nestability before you commit to anything.

Own the Sun. Not the Risk.™