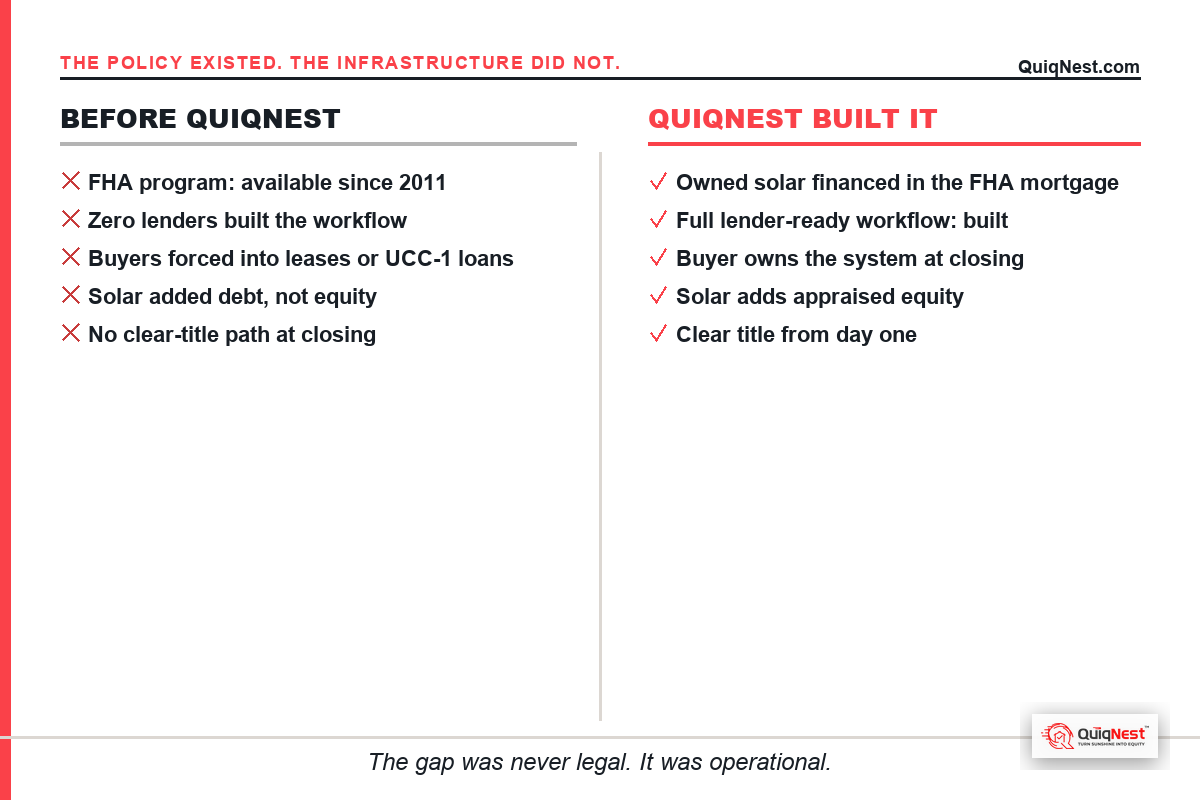

The FHA Solar and Wind Technologies provision sits in HUD Handbook 4000.1, Section II.A.8.a. It has been there since 2011. It allows any FHA-approved lender to include the cost of a new owned solar system in the base loan amount at purchase. No specialty designation required. No new program approval needed. Any lender with an existing FHA approval can originate it today.

For 13 years, almost nobody used it. Not because the policy was wrong. Not because solar was not a mature technology. Not because buyers did not want it. Because the workflow to deliver it at scale did not exist.

The gap was operational

To originate solar inside a purchase mortgage at closing, a lender needs four things: a solar assessment process that runs before the appraisal, an installer who provides a cost estimate in the format the lender requires, a compliance layer keeping the transaction within FHA program parameters, and a post-closing installation workflow tied to the escrow holdback the program requires.

None of those pieces are individually complex. Together, as a coordinated workflow, they did not exist in a form any lender could use. So lenders defaulted to what was easy: leases where a third party retains ownership, and UCC-1 loans where a separate lender holds a security interest against the home. Both put solar on the roof. Neither gives the buyer a clear-title asset.

QuiqNest built the missing workflow

The solar assessment. The installer coordination. The compliance layer. The post-closing installation process tied to the escrow holdback. Delivered as infrastructure an FHA-approved lender can use without rebuilding their origination stack.

The policy existed. The market existed. The demand existed. The workflow was the gap. We closed it.