You closed on your first home in the winter or the spring. The first few months felt manageable. The power bill looked roughly like what you were used to, and you started to relax.

Then summer arrived.

The air conditioning began running the way it runs in a house, not the way it ran in an apartment. The first real summer bill landed, and it was nothing like anything you paid as a renter. The immediate assumption, the one almost every first-time homeowner has, is that something must be wrong.

Usually nothing is wrong. The bill is simply the first honest measurement of what it costs to own a home, instead of rent one, through a hot summer.

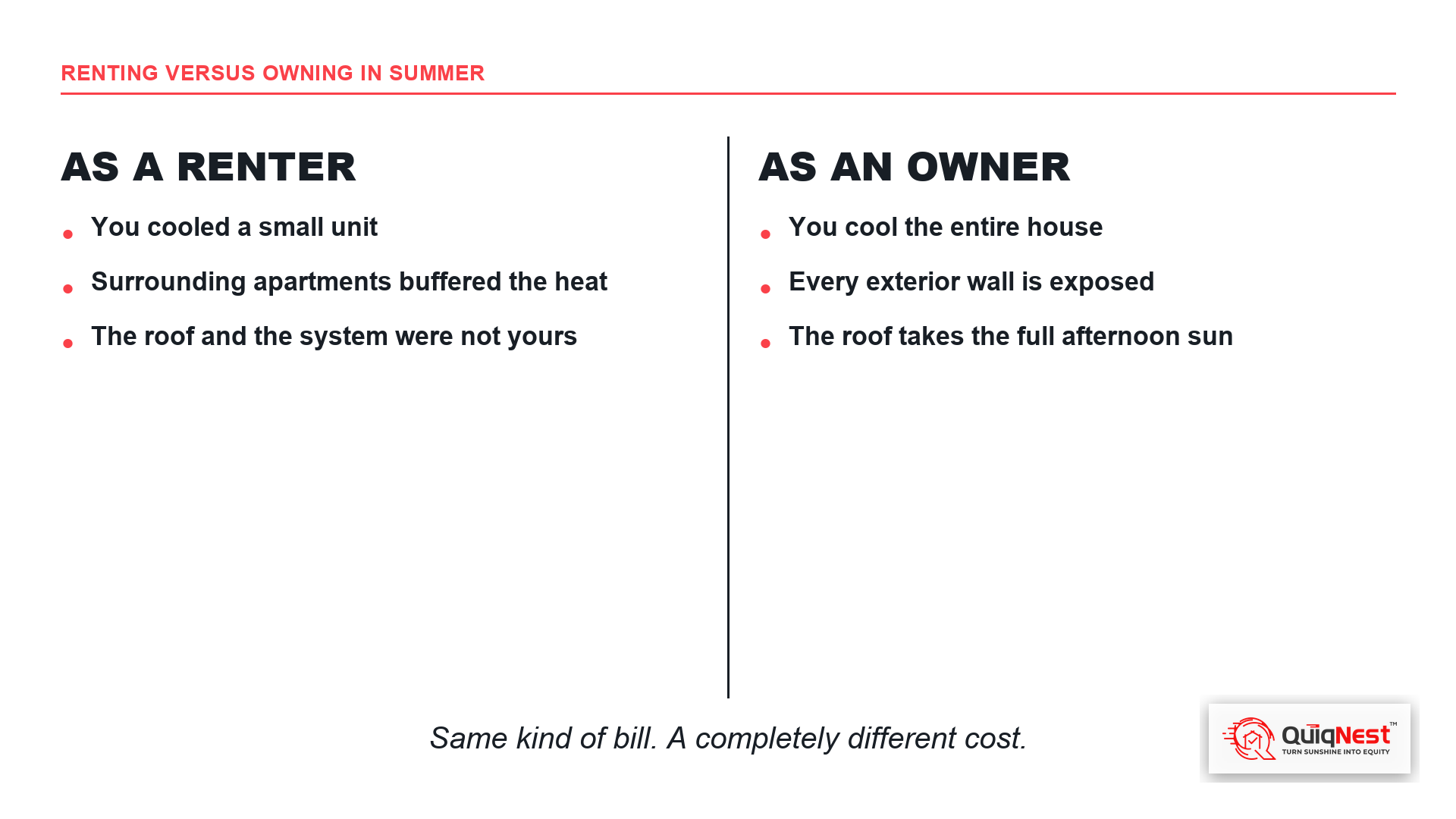

A renter's bill and an owner's bill are different animals

The jump between renting and owning catches first-time buyers off guard because the two situations are not comparable, even though they both arrive as an electric bill.

You used to cool a small space. As a renter, you were most likely conditioning a one-bedroom or two-bedroom unit. Now you are cooling an entire house, with more rooms, more air volume, and often higher ceilings. The system has more work to do, and it does that work all summer.

The building used to protect you. In a multi-unit building, the apartments around you act as insulation. Shared walls, the unit above, and the unit below all buffer heat transfer. A middle-floor apartment is shielded on several sides. A house is exposed on every side, with exterior walls all around and a roof directly overhead.

The roof was not your problem. As a renter, you almost certainly never thought about the building's roof. As a homeowner, the roof is yours, and in a hot climate the roof is where a large share of the cooling load comes from. Through every summer afternoon, the sun bears down on it, and your air conditioning works against everything that roof absorbs.

You inherited someone else's system. A renter relies on whatever cooling system the landlord installs and maintains. A homeowner inherits whatever the builder or the previous owner chose, and lives with its efficiency, or its lack of efficiency, on every monthly bill.

The bill is honest. The closing process was incomplete.

Put those factors together and the steep first-summer bill stops looking like an error. It is the accurate cost of cooling a whole house, under its own roof, with the system you inherited.

What makes it feel like a shock is not the bill itself. It is that nothing in the homebuying process prepared you for it. The closing process is thorough about almost every cost of the home. Property taxes are disclosed and built into escrow. Homeowners insurance is disclosed and built into escrow. Every closing cost appears as a line item.

The summer power bill has none of those forcing functions. No authority sets it in advance. No lender escrows it. No federal form itemizes it for the buyer. So it falls into a gap, and the first-time buyer discovers it the hard way, in July, with the air conditioning running.

The bill becomes a decision

For most first-time homeowners, the high summer bill does not stay an annoyance. It becomes the reason they start thinking seriously about solar. The bill arrives, the math feels urgent, and within a few weeks a solar company has them on a quote.

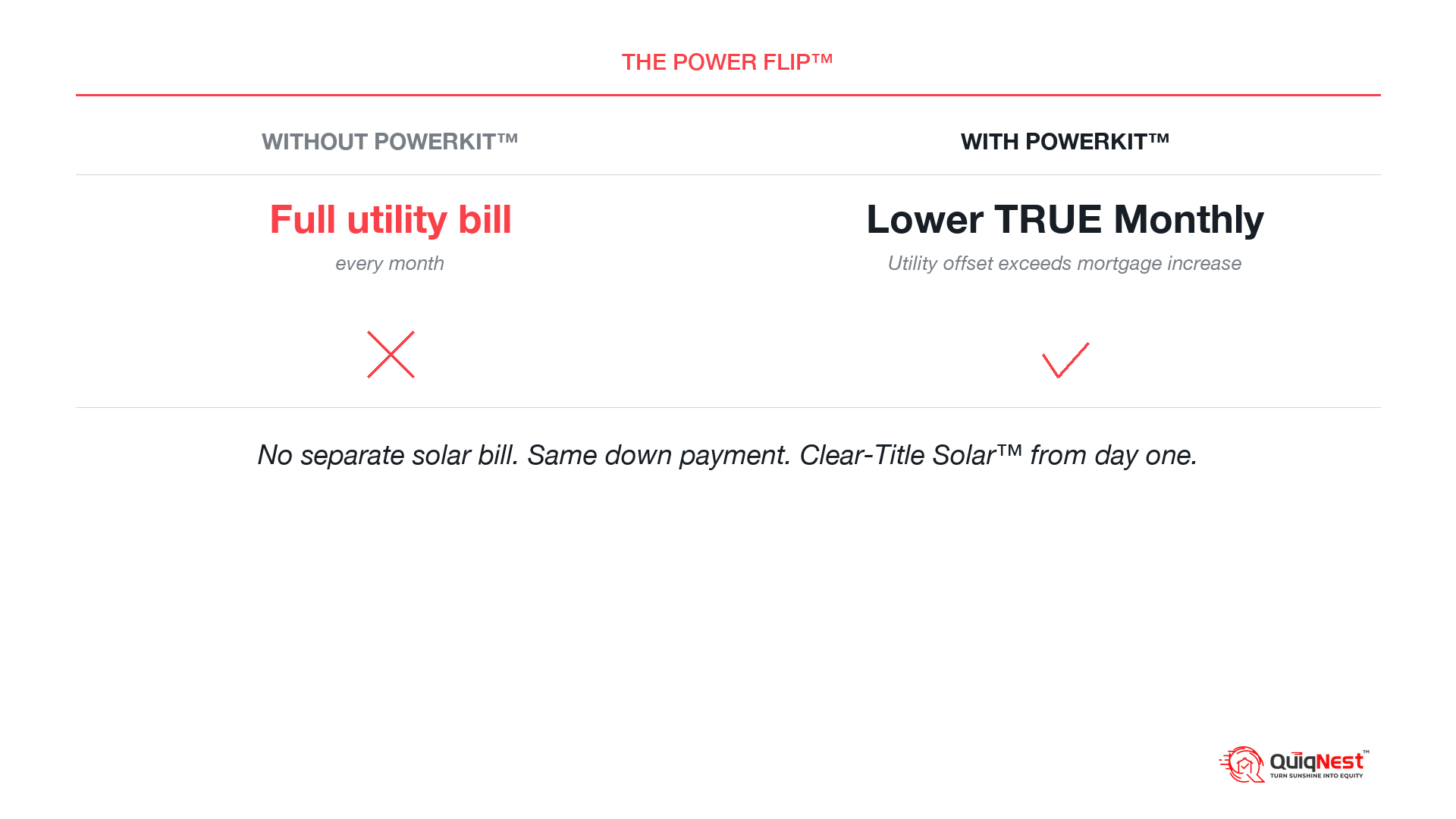

This is the moment that matters more than the bill. Because the homeowner is now making a financing decision, and the financing path will decide whether solar becomes an asset that builds equity or a liability that has to be managed around at the next refinance or sale.

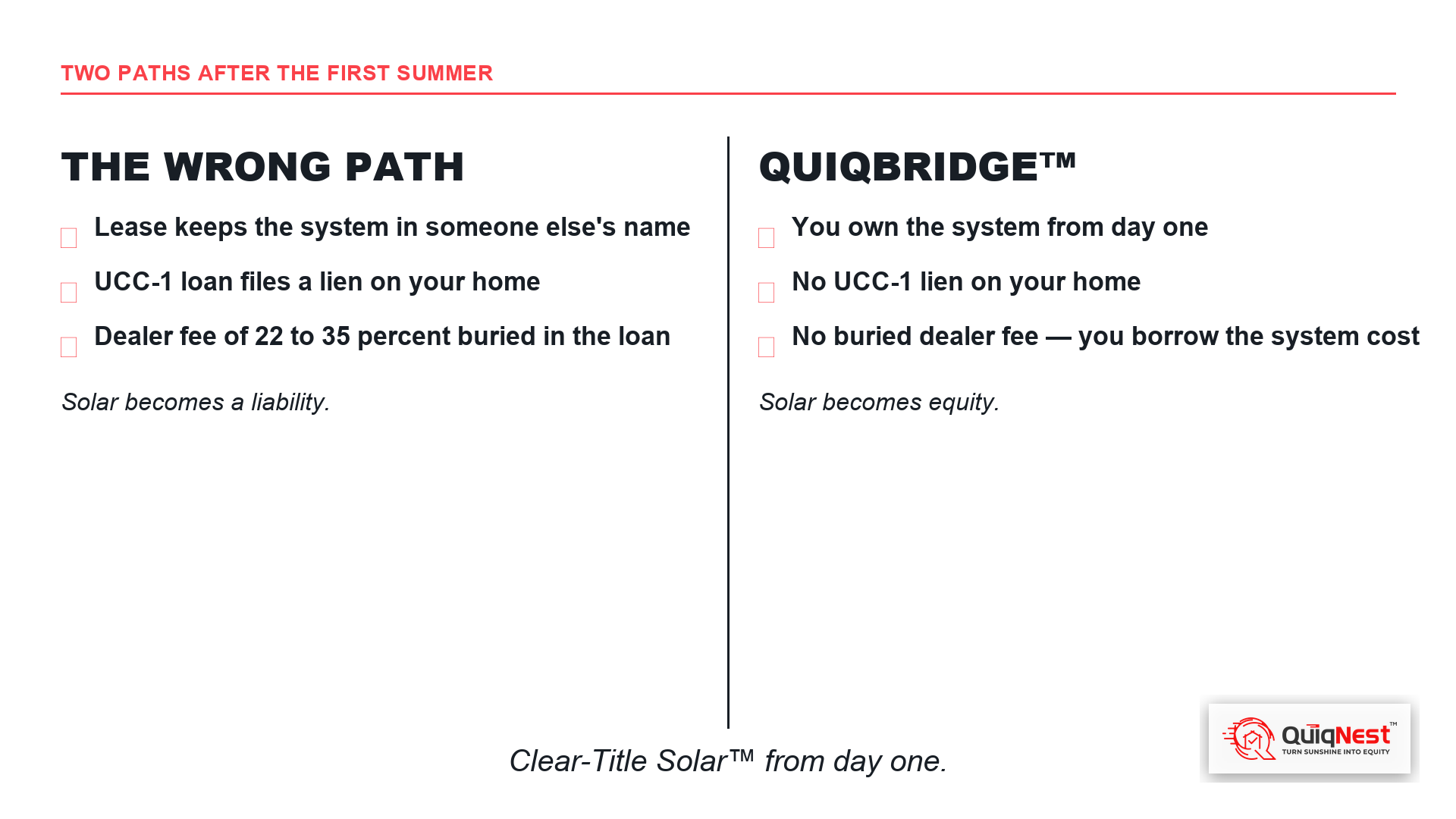

Most first-time buyers get pushed toward one of two paths.

A solar lease puts panels on the roof, but the system stays in the leasing company's name for a 20 to 25 year term. The homeowner does not own the asset, and the home receives no contributory value for it.

A UCC-1 solar loan lets the homeowner buy the system, but the lender files a UCC-1 financing statement, which places a lien on the home. These loans also commonly bury a dealer fee of 22 to 35 percent inside the loan principal. A system that costs $25,000 becomes a financed balance closer to $33,750.

Both paths solve the summer bill. Both create a new problem that surfaces later, at the title company.

The path that builds equity

QuiqBridge™ from QuiqNest gives recent first-time buyers a third path.

With QuiqBridge™, the homeowner installs solar now and owns it from day one. There is no UCC-1 lien on the home and no buried dealer fee. The amount borrowed matches the system cost. The result is Clear-Title Solar™ from the moment the system is installed, structured to convert cleanly into the primary mortgage through QuiqRefi™ when equity or rate conditions support it.

It is built for a specific homeowner: someone who closed in the last 3 to 12 months, does not have meaningful equity yet, and wants solar without inheriting a 25-year structural problem. Available in Florida and Texas, for systems up to $25,000, with terms up to 20 years and no equity required to start.

The warning you did not get

Nobody warned you about the first summer. That gap in the homebuying process is not going to close on its own.

What you can control is what happens next. The summer bill is the trigger. The financing path is the decision. One path turns solar into equity in the first home you worked hard to buy. The other turns it into a lien you will be explaining to a title company years from now.

If you closed in the last 3 to 12 months and the first summer is the reason you are reading this, run the Power Flip on your home at QuiqNest.com and see what the QuiqBridge™ path looks like on your actual address.