When you tour a new construction home with solar panels on the roof, the natural assumption is that the solar comes with the house, the way the appliances do, the way the warranty does, the way the landscaping does.

Sometimes that assumption is correct. Sometimes it is not. And the difference between the two is one of the most consequential financial facts about the home you are considering, one that almost never comes up at the model home.

Here is what is actually happening, and why it matters on November 2, 2026.

The builder made the solar decision before you arrived

When a builder partners with a solar company to include solar in a new community, the structure of that arrangement is set long before the first buyer tours the model. The builder and their solar partner agreed on a product, a pricing structure, and a contract. By the time you are standing in the kitchen of the model home looking at the energy cost estimates on the sales brochure, the decision about who owns those panels has already been made.

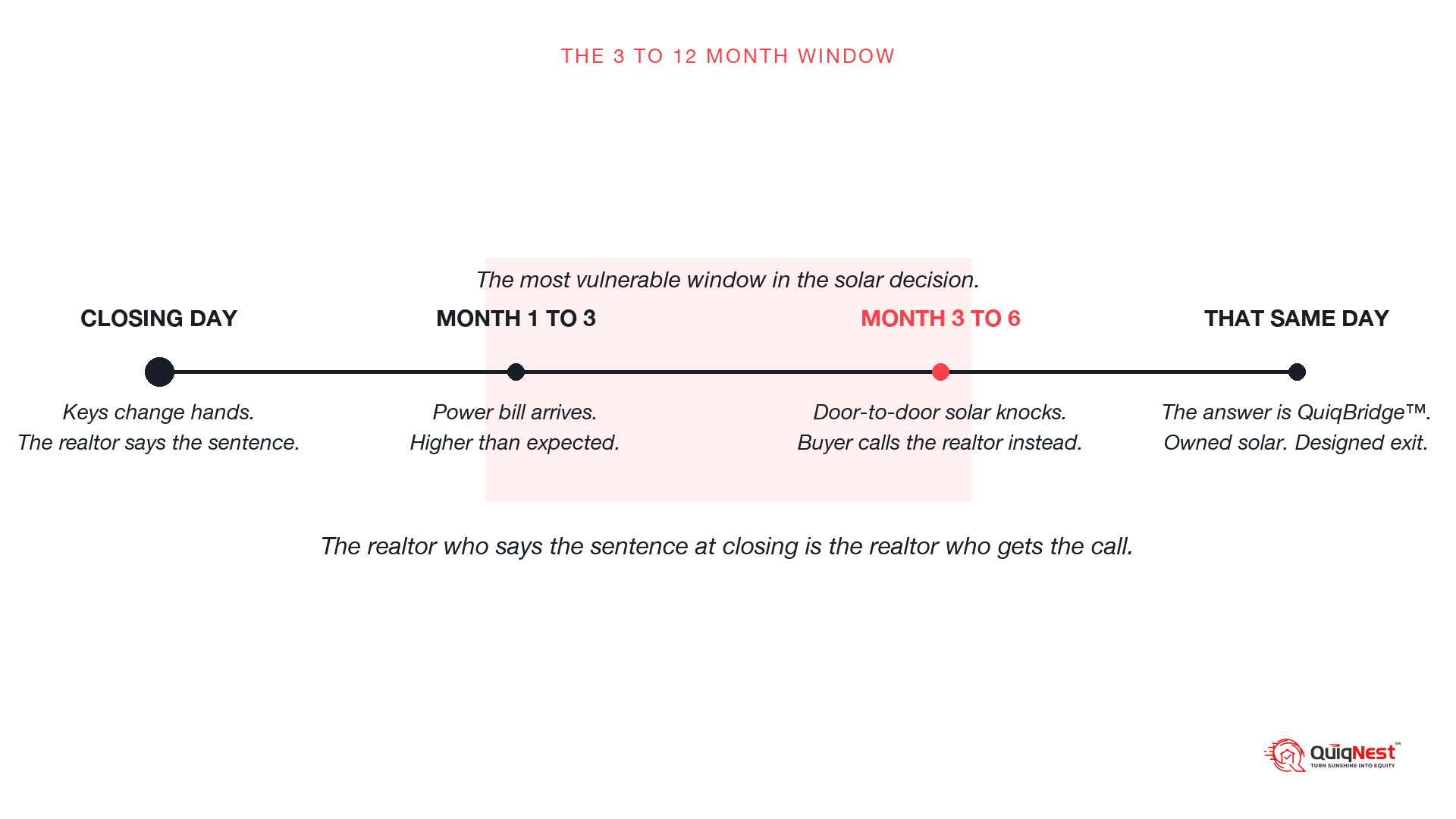

Most buyers never ask about it. The sales agent mentions the solar as a feature. The brochure shows estimated monthly savings. The conversation moves on. Nobody at the model home explains that the solar package comes in two fundamentally different structures with completely different financial outcomes.

The two structures

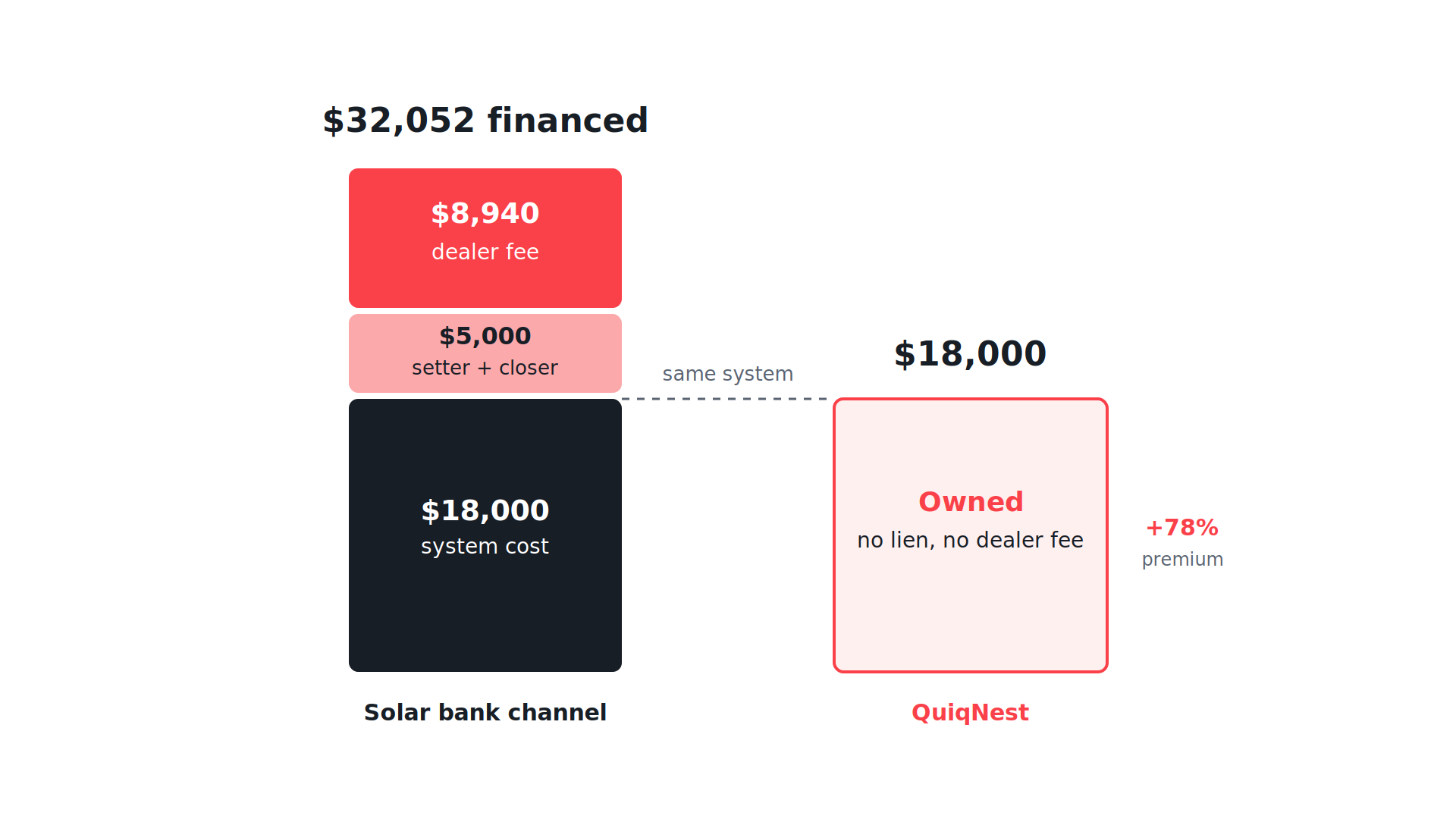

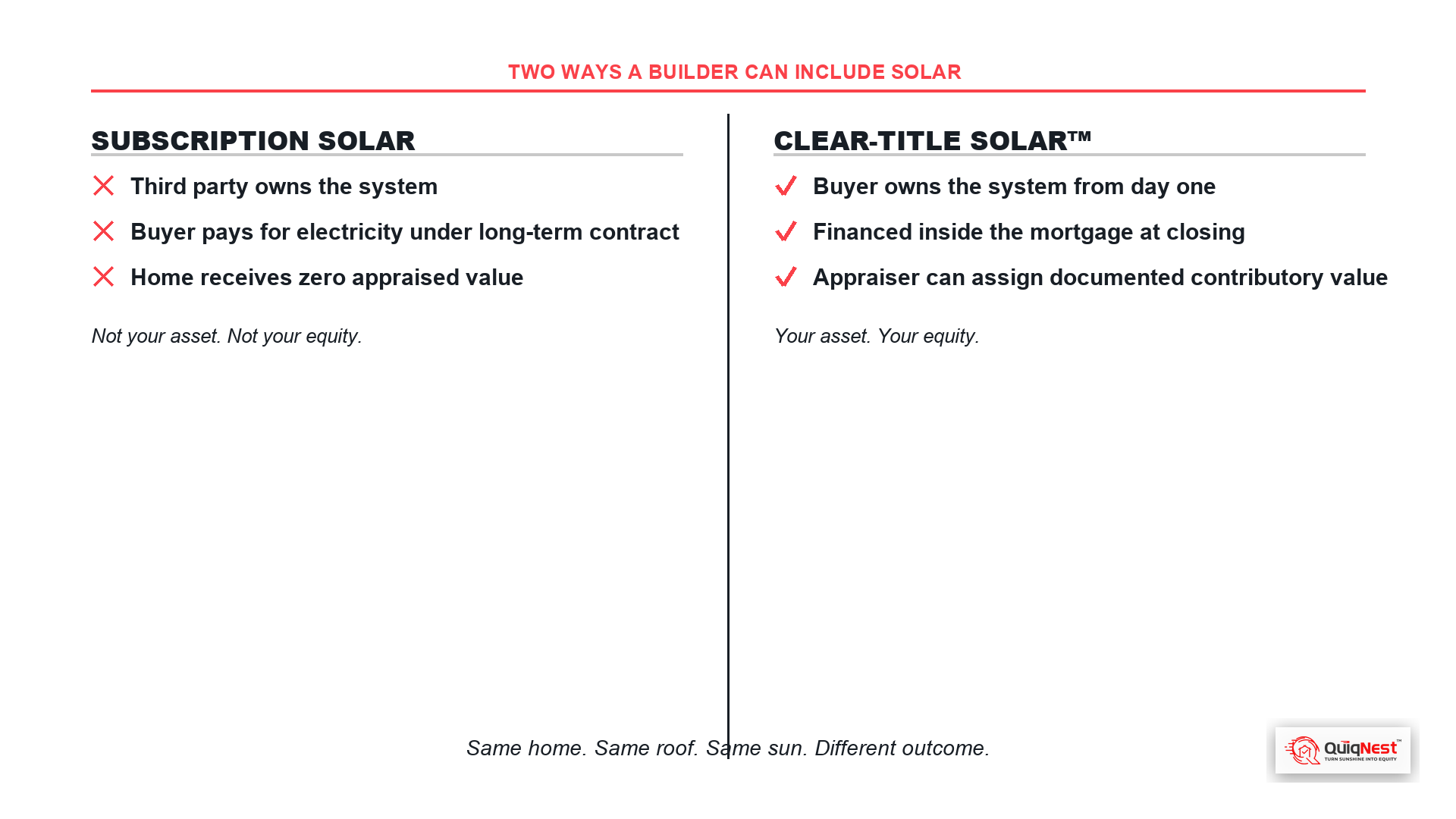

Subscription or lease solar. In this structure, a third-party company owns the solar system. The panels sit on the roof of the home, but they are not part of the real property. The buyer signs a contract to pay for the electricity the system produces, typically for 10 years with a 3-year minimum, on terms that were set before the buyer was ever involved.

The home receives no appraised value for those panels. Under residential appraisal policy, equipment owned by a third party that can be repossessed or removed cannot add contributory value to the home. The appraiser is valuing the home and its permanent features, not a contractual relationship with a company that retains title to the equipment.

Owned solar, financed inside the mortgage. In this structure, the solar system is purchased by the buyer and financed inside the purchase mortgage at closing. The buyer owns the system from day one of ownership. There is no subscription contract and no third-party lien on the title. The system is a clear-title asset, the same way the roof is a clear-title asset.

The appraiser can assign documented contributory value to an owned solar system. The system adds to the home's appraised value. The equity the buyer builds from closing onward includes the solar.

What changes on November 2, 2026

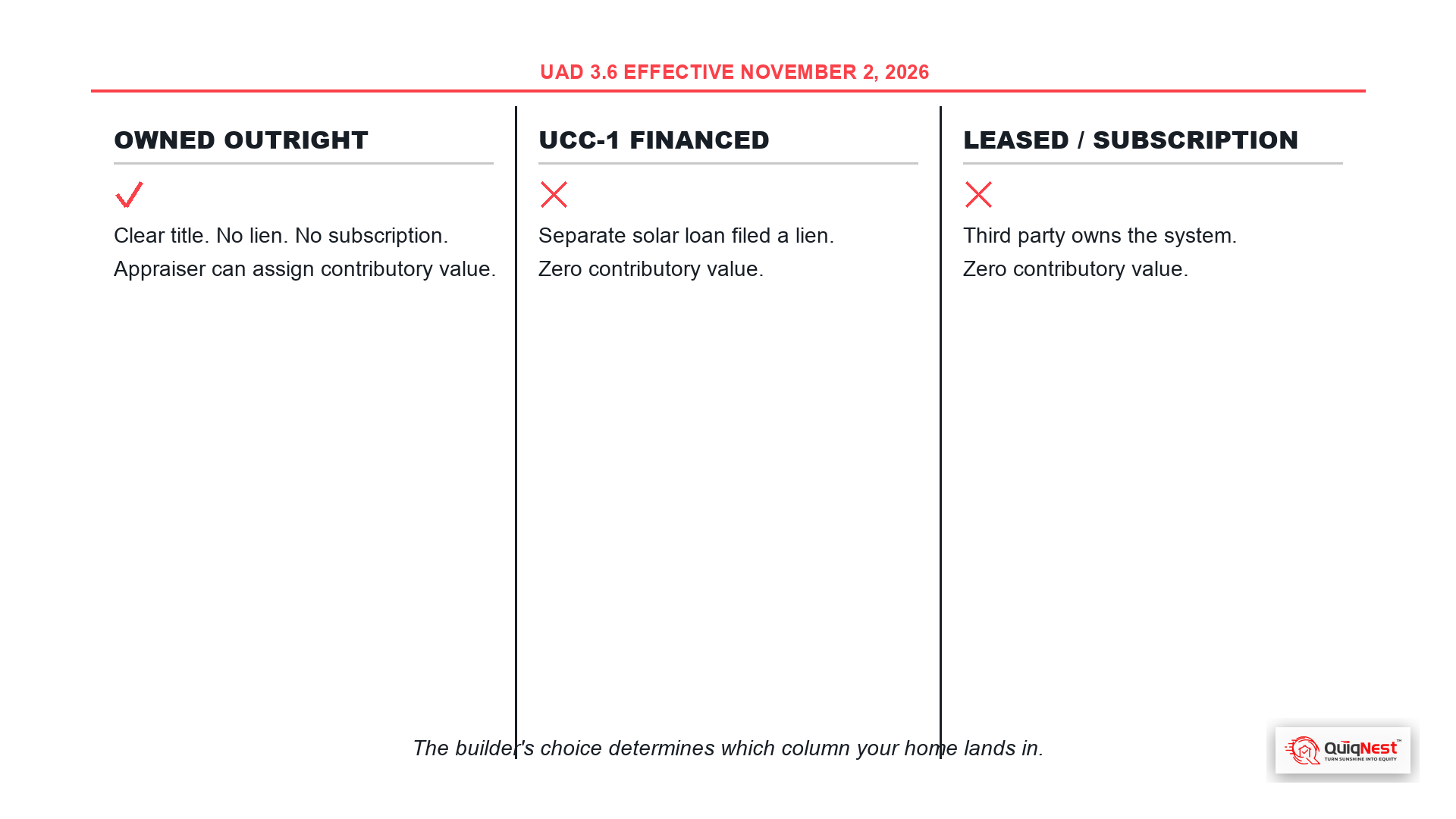

On November 2, 2026, UAD 3.6 takes effect. It is the largest update to residential appraisal standards in over 15 years.

The mandate converts solar from a narrative appraisal field into structured, machine-readable data. Section 6 of every Fannie Mae and Freddie Mac appraisal will report solar in one of three structured categories. Owned outright. Financed with UCC-1 lien. Leased or subscription.

The third category, leased or subscription, is explicitly the category that carries zero contributory value. The data flows directly into automated underwriting systems, pricing models, and risk analysis. The distinction between owned and subscription solar, which has always existed in appraisal policy, becomes visible at every level of the mortgage system simultaneously.

A new construction home delivered with subscription solar will, after November 2, appraise with zero solar value. The same home delivered with owned Clear-Title Solar™ carries an asset the appraiser can document and defend.

The builder's choice, made before the first buyer toured the model, determines which of those two outcomes every buyer in that community inherits for the life of the home.

Why this matters for a buyer specifically

As a buyer, you are making a 30-year financial decision when you buy a home. The appraisal at closing is the first moment that decision gets measured. But it is not the last. The home will be appraised again at every refinance and every resale.

If the solar on your new construction home is a subscription, it adds nothing to any of those appraisals. It is not an asset you own. It does not build equity. It does not offset the cost of the home in any way the mortgage system can measure.

If the solar is owned and financed into your mortgage, it is part of the home you are building equity in from day one. On a correctly sized system, the energy offset lowers your total monthly cost below what the same home would cost without solar. The system adds to the home's appraised value at every future measurement point.

Same roof. Same sun. The structure of the solar determines the outcome.

What Solar-Ready Homes™ from QuiqNest offer

Solar-Ready Homes™ from QuiqNest are new construction homes where solar is financed inside the FHA mortgage at closing through BrightNest Mortgage™. The buyer's down payment does not change. There is no subscription contract and no third-party lien on the title. The system is installed after closing and is owned by the buyer from day one of ownership.

The four-line outcome is consistent regardless of the specific home or market.

Same cash to close. The solar is inside the mortgage, so the down payment stays the same as the same home without solar.

Lower monthly. On a correctly sized system the energy offset exceeds the marginal mortgage increase.

Higher home value. Owned solar is the only structured category positioned to add documented contributory value under UAD 3.6.

No appraisal gap. Because solar is installed after closing, there is no second appraisal step that creates a gap between the purchase price and the appraised value.

The question to ask at the model home

If you are touring new construction in Florida, the question is simple. Who owns the solar system on this home. Is it financed into the mortgage, or is it a subscription contract with a third-party company.

If the answer is a subscription, you are inheriting someone else's equipment on your roof, a long-term contract you did not negotiate, and zero appraised value for any of it.

If the answer is owned and financed into the mortgage, you are buying a clear-title asset from day one.

Browse Solar-Ready Homes™ across Florida and check any address before your next new construction tour at quiqnest.com/solar-ready-homes.