For two years, the team at QuiqNest has been building the infrastructure layer for solar inside the mortgage.

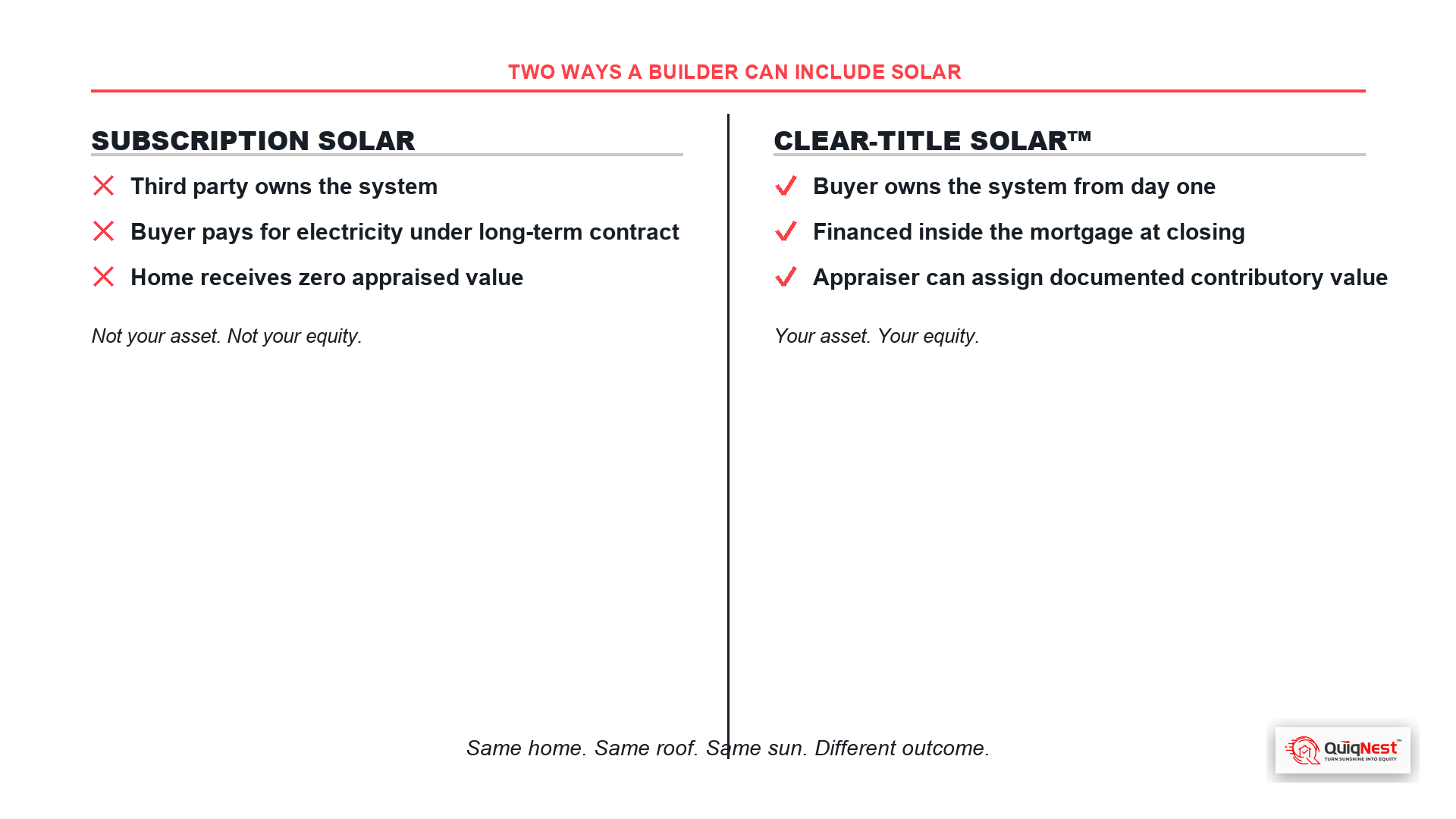

The category we have been building is called Clear-Title Solar™. The defining feature of the category is what it does not have. No UCC-1 lien on the home. No lease agreement attached to the panels. No third party with the right to repossess, terminate, or take back the equipment. No second appraisal step that bolts on after closing.

We named the category for the absence, because the absence is the entire point.

This is a founder's note on what we built, why we built it, and what the moment between now and November 2, 2026 means for anyone in the path of residential mortgage, real estate, or solar finance.

The problem we kept seeing

For more than a decade, the residential solar industry has run on two financing structures.

Solar leases. A third party owns the panels. The homeowner pays for the electricity under a long-term contract, usually 20 or 25 years. The lease company holds the right to terminate, remove, or transfer the equipment. The home does not receive credit for the panels in any appraisal that follows residential appraisal policy correctly.

Solar loans with UCC-1 financing statements. The homeowner takes a separate solar loan from a non-mortgage lender. The lender files a UCC-1 financing statement under Article 9 of the Uniform Commercial Code, attaching a security interest to the panels and, in many filings, to the home itself. The lien shows up in any title search. The home does not receive contributory value credit, because the panels can be repossessed by the lender in default.

Both structures share a foundational problem. Inside Fannie Mae and Freddie Mac appraisal policy, equipment that a third party can repossess, terminate, or take back from the home cannot add contributory value to the home in the appraisal. The principle is older than residential solar. The principle has been quietly costing homeowners with the wrong kind of solar for years.

The reason the principle has not been widely understood is that residential appraisals before UAD 3.6 used narrative language. Appraisers wrote sentences. Underwriters read sentences. The data was inconsistent across appraisers, lenders, and markets. The truth was visible inside the policy but not inside the data that AUS, underwriting, and pricing read.

On November 2, 2026, that changes.

What UAD 3.6 actually does

UAD stands for Uniform Appraisal Dataset. Version 3.6 replaces the narrative fields of earlier versions with structured, machine-readable data fields. Section 6 of every Fannie Mae and Freddie Mac appraisal will report solar in one of three structured categories.

Owned outright. The homeowner owns the system free and clear. No lien. No lease. The appraiser can assign documented contributory value.

Financed with UCC-1 lien. The system was purchased with a separate solar loan that filed a UCC-1 financing statement. The lender holds a security interest. The structured field reports the lien. The home does not receive contributory value credit.

Leased or PPA. A third party owns the system. The homeowner pays for the electricity under a long-term contract. The structured field reports the lease. The home does not receive contributory value credit.

The data flows into AUS, underwriting review, and risk pricing. Information that previously surfaced during title work or appraisal review now surfaces earlier in the cycle. The fluency advantage that informed buyers, agents, and lenders have today becomes a competitive advantage that compounds every time a transaction touches a home with solar on it.

This is the largest update to residential appraisal standards in over 15 years.

What we built

QuiqNest exists because the obvious answer to the contributory value rule has always been the same. If equipment that a third party can take back cannot add value to a home, then the path to solar that adds value is solar the homeowner owns, with no third party that can take it back.

For a homebuyer, the cleanest way to own solar is to finance it inside the same mortgage that finances the home. No separate solar loan. No UCC-1. No lease. The system is owned from day one. The home appraises as-is at closing. Solar is installed after closing.

That is BrightNest Mortgage™.

The buyer's down payment stays the same as the same home without solar. The closing costs stay the same. The monthly mortgage payment increases by the marginal cost of the solar financed inside the mortgage. The monthly utility cost decreases by the production of the solar system. The net of those two numbers, when the system is sized correctly for the home and the household, is a lower total monthly cost than the same home without solar.

The four-line value proposition we have used across every day of this campaign is the direct consequence of that structure.

Same cash to close. Lower monthly. Higher home value. No appraisal gap.

Each of those four lines maps to a structural feature of BrightNest Mortgage™. Same cash to close, because solar is rolled into the FHA mortgage without changing the down payment or the closing costs. Lower monthly, because the energy offset on a correctly sized system exceeds the marginal mortgage increase. Higher home value, because owned solar is the only structured category positioned to receive documented contributory value going forward. No appraisal gap, because the home appraises as-is at closing and solar is installed after, eliminating the second appraisal step that any after-market solar installation would trigger.

For homeowners who already closed

BrightNest Mortgage™ is built for buyers who have not closed yet. There is a separate audience that the category serves, and we built a separate product for them.

If you closed on a home in the last 3 to 12 months and you are now thinking about solar, the situation usually looks like this. You bought the home. The summer hit. The utility bill arrived. A solar dealer knocked on the door or sent you a quote. The quote was for a UCC-1 financed solar loan or a 25-year lease.

Both of those products move you into one of the two structured UAD 3.6 categories that have always failed the contributory value test. The dealer fee buried in a typical solar loan turns a $25,000 system into a $33,750 loan. The lease ties you to a long-term contract a future buyer will be asked to assume.

You do not have meaningful equity yet, so a cash-out refinance is not the answer either.

This is the gap we built QuiqBridge™ for. QuiqBridge™ finances owned solar with no UCC-1 lien, no buried dealer fee, and a structure designed to refinance cleanly into your primary mortgage later when equity or rate conditions support it. The end state is Clear-Title Solar™. Owned. Clean. Equity-building. Resale-ready.

QuiqBridge™ is available in Florida and Texas. System financing up to $25,000. Term up to 20 years. Minimum credit around 640. Equity required to start: none.

If you closed years ago and have built equity, QuiqRefi™ is the better path. If you have not bought yet, BrightNest Mortgage™ is the better path. If you already have leased solar or UCC-1 financed solar on your roof, QuiqBridge™ is not the right tool. We will say that directly, because we built the category for honest matches.

What this means for everyone else in the path

For real estate agents, the structured fields are about to change which listings move quickly and which slow down. Listings with owned solar and no separate lien defend at higher price points more cleanly. Listings with UCC-1 financed solar and listings with leased solar carry friction the buyer's lender will surface earlier. Agents who learn the three categories in May are agents whose listings sell in November.

For loan officers and originators, the underwriting system reads the structured fields directly. UCC-1 financed solar surfaces in DU and LPA automatically. Leased solar triggers the assumption review path automatically. Cycle times extend on both. The originator who can offer a buyer the clean path to owned solar inside the mortgage at purchase is the originator who closes the deal a competing lender cannot.

For builders, inventory closing in Q4 2026 is being priced now. Builders aligning with BrightNest Mortgage™ in summer are positioned to deliver homes that close cleanly under UAD 3.6. Builders who do not align are pricing inventory against a market that has changed underneath them.

For solar partners, the EPCs and installers aligning with mortgage-integrated solar in summer 2026 are the partners positioned for the back half of 2026 and into 2027. The ones who continue running the UCC-1 solar loan playbook are the ones whose lead flow tightens.

None of this is dramatic. It is structural. The same way every other federal data-standard change has played out in residential mortgage.

What we are not

We are not a solar company. We do not sell panels. We do not knock on doors. We do not run a UCC-1 solar loan book.

We are an infrastructure layer. We build the products that let mortgage lenders originate Clear-Title Solar™ inside their normal workflow. We work with approved lender partners and certified installer partners who meet our standards for the category. We make the math runnable on any address in 30 seconds through the Power Flip™.

The Power Flip™ is the surface most people meet QuiqNest through. It is free. It runs on any address. It returns the financial picture of what owned solar inside the mortgage looks like on that specific home, with the buyer's down payment held constant.

If you have read this far, the Power Flip is the next step. Open a tab to QuiqNest.com, type in an address you are considering, and let the math run.

What's the Power Flip on your next home?

We have spent two years building this category because we believe owned solar inside the mortgage is the only version of residential solar that survives the next 10 years of appraisal policy, regulatory clarity, and consumer expectation cleanly.

The four-line value proposition is the proof.

Same cash to close. Lower monthly. Higher home value. No appraisal gap.

The companies, agents, and lenders talking about this in May will be the ones people trust in November.

This is what owning the sun looks like.

Patrick Blanchet

Founder, QuiqNest