For more than a decade, homeowners with leased solar have run into the same wall.

They go to refinance. The appraiser walks the home, notes the panels, and assigns zero contributory value. The lease stays on the books. The refinance numbers do not work the way the original solar dealer suggested they would.

Or they go to sell. The buyer's lender flags the lease. The buyer is asked to assume the lease or buy out the contract. The transaction slows. Sometimes it dies.

This pattern is not new. Appraisers, real estate attorneys, and lender underwriters have known about it for years. What is new is that on November 2, 2026, the entire residential mortgage system in America is going to start saying it out loud, in machine-readable data, on every single appraisal.

The mandate is called UAD 3.6. It is the largest update to residential appraisal standards in over 15 years.

What UAD 3.6 actually does

UAD stands for Uniform Appraisal Dataset. Versions 2.6 and earlier used narrative language to describe property features, including solar. Appraisers wrote sentences. Underwriters read sentences. The data was inconsistent across appraisers, lenders, and markets.

UAD 3.6 replaces narrative with structured data fields. Section 6 of every Fannie Mae and Freddie Mac appraisal will report solar in one of three structured, machine-readable categories.

The first is owned outright. The homeowner owns the solar system free and clear. No lien, no lease. The second is financed with a UCC-1 lien. The system was bought with a separate solar loan that filed a UCC-1 financing statement against the panels and the home as collateral. The third is leased or PPA. The system is owned by a third party. The homeowner pays for the electricity it produces under a long-term contract.

The data is now machine-readable. It feeds the same systems that support automated underwriting, risk analysis, and pricing.

Why this matters if you are buying a home in 2026

If you are shopping for a home this year, the structured fields are about to change which homes are easy to finance and which are not.

Owned solar will be straightforward. The appraiser documents the contributory value. The title is clean. The closing moves at standard speed.

UCC-1 financed solar will be visible to underwriting in a way it was not before. The lien shows up on the title search. Closings slow by 10 to 30 days while the seller works to subordinate or terminate the lien. Some deals do not survive the delay.

Leased solar will trigger the assumption conversation earlier. The buyer's lender sees the structured field. The buyer is asked to assume the lease or buy it out before underwriting clears the loan.

The clean path is to skip all three problems entirely by financing owned solar inside the mortgage itself.

That is what BrightNest Mortgage™ does. The system is financed inside the FHA mortgage at purchase. The buyer owns the panels from day one. There is no separate solar loan and no UCC-1 lien on the title. The home appraises as-is at closing. Solar is installed after closing. Same cash to close, lower monthly payment, higher home value, and no appraisal gap.

Why this matters if you just bought your home

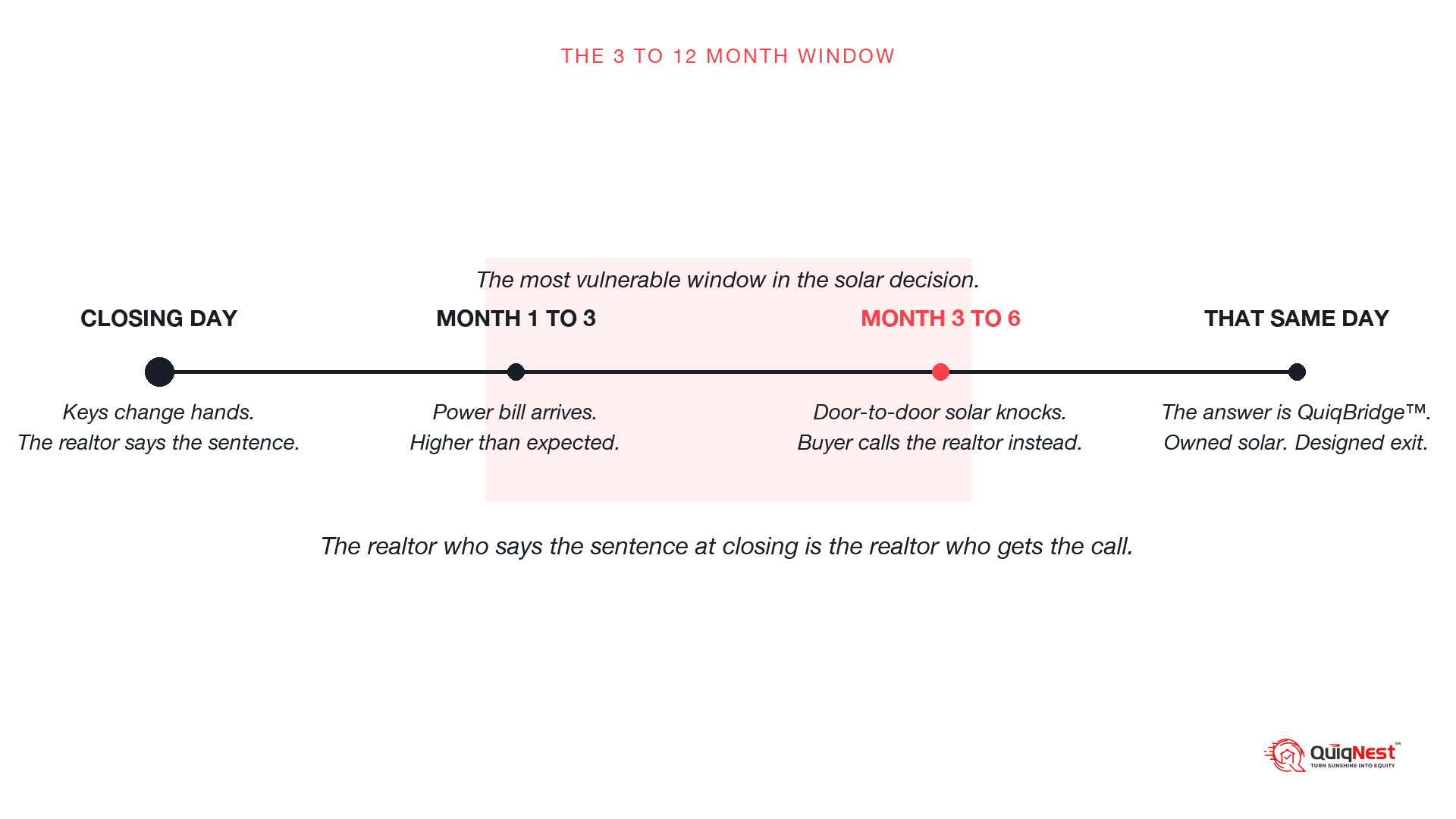

There is a specific group of homeowners this update affects in a sharper way: the people who closed on a home in the last 3 to 12 months and are now thinking about solar.

If that is you, the situation usually looks like this. You bought the home. The summer hit. The utility bill arrived. A solar dealer knocked on your door or sent you a quote. The quote was for a UCC-1 financed solar loan or a 25-year lease.

Both of those products move you into one of the two structured UAD 3.6 categories that have historically appraised at zero. The dealer fee buried in a typical solar loan turns a $25,000 system into a $33,750 loan. The lease ties you to a 25-year contract that future buyers will be asked to assume.

You do not have meaningful equity yet, so a cash-out refinance is not the answer either.

This is the gap QuiqBridge™ was built for. QuiqBridge™ finances owned solar with no UCC-1 lien, no buried dealer fee, and a structure designed to refinance cleanly into your primary mortgage later, when equity or rate conditions support it. The end state is Clear-Title Solar™. Owned. Clean. Equity-building. Resale-ready.

QuiqBridge™ is available in Florida and Texas. System financing up to $25,000. Term up to 20 years. Minimum credit around 640. Equity required to start: none.

It is specifically for homeowners who closed 3 to 12 months ago. If you closed years ago and have built up equity, QuiqRefi™ is a better path. If you have not bought yet, BrightNest Mortgage™ is a better path. If you already have leased solar or UCC-1 financed solar on your roof, QuiqBridge™ is not the right tool.