The closing table is one of the most thorough hours in the entire homebuying process.

A settlement agent walks you through the property taxes. Through the homeowners insurance. Through the escrow account that will hold both. Through the interest rate, the loan terms, and every closing cost, line by line, until you have signed your name more times than you can count.

By the end of that hour, you have a clear and detailed picture of almost every dollar the home will cost you.

There is one large, recurring cost that hour never covers. The power bill.

The cost the process forgets

Property taxes are disclosed because a public authority sets them and a lender escrows them. Homeowners insurance is disclosed because a lender requires it and escrows it. Closing costs are disclosed because federal rules require an itemized settlement statement.

The power bill has none of those forcing functions. No authority sets it in advance. No lender escrows it. No federal form itemizes it for the buyer. So it falls into a gap. It is one of the largest ongoing costs of owning a home, and the buying process does almost nothing to prepare you for it.

The previous owner might have mentioned a number in passing. A listing might have noted average utilities. But a number from a different household, with different habits, different thermostat settings, and a different tolerance for being slightly too warm or slightly too cold, is not a number you can budget against.

So most buyers do not budget against it. They close, they move in, and they wait to find out.

Why the bill is so high in a new home

When the first full season of occupancy arrives and the bill shows up, it is often far higher than anything the buyer imagined. This is not bad luck and it is not a defect in the home. It is the predictable result of what is selling well in the current market.

More square footage. Larger homes have more air volume to heat and cool. A move-up buyer going from a smaller home to a larger one often sees the energy cost rise faster than the square footage did, because conditioning a larger space is not a linear cost.

All-electric construction. Many newer homes are built all-electric. There is no gas line splitting the energy load. Heating, cooling, water heating, cooking, and everything else lands on a single electric bill. The total cost of running the home is concentrated into one number, and that number looks alarming even when the home is reasonably efficient.

Builder-grade systems. New construction meets code. Code is a minimum, not an optimization. A builder-grade HVAC system and builder-grade insulation will pass inspection and still run harder and longer than a system chosen specifically to minimize operating cost.

No mature landscaping. A newly built home usually comes with young trees and small plantings. Mature shade trees can meaningfully reduce cooling load in a hot climate. A new home does not have them, and will not for years, so the home absorbs full sun on its roof and walls through every summer afternoon.

None of these are problems with your home. They are simply the real operating cost of the home, arriving after the keys, in a bill the closing process never asked you to plan for.

The bill becomes a decision

For most new homeowners, the high power bill does not stay an annoyance. It becomes the trigger for a solar conversation. The bill arrives, the math feels urgent, and within a few weeks a solar company has the homeowner on a quote.

This is the moment that matters more than the bill itself. Because the homeowner is now making a financing decision, and the financing path will determine whether solar becomes an asset that builds equity in the home or a liability that has to be managed around at the next refinance or sale.

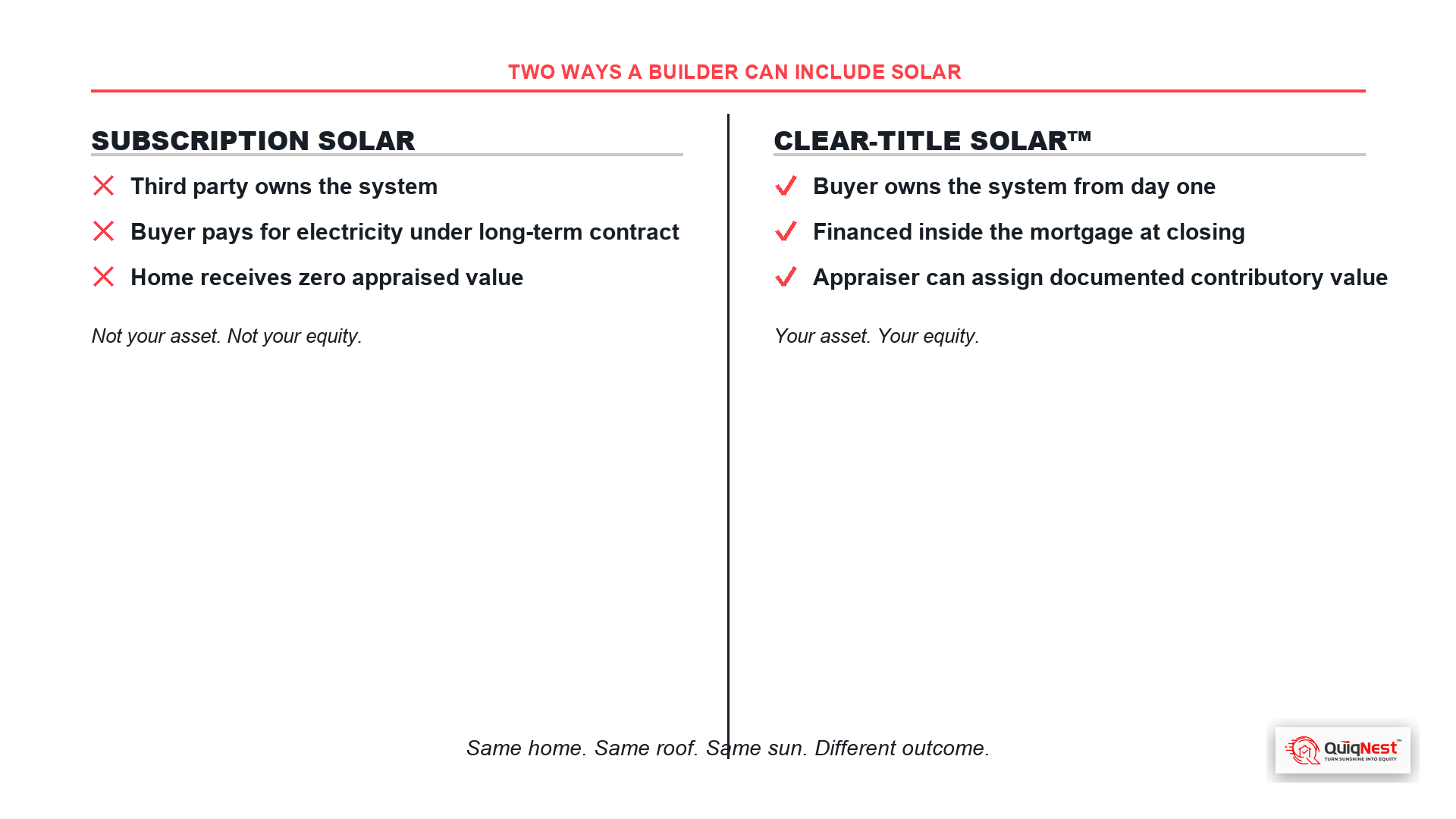

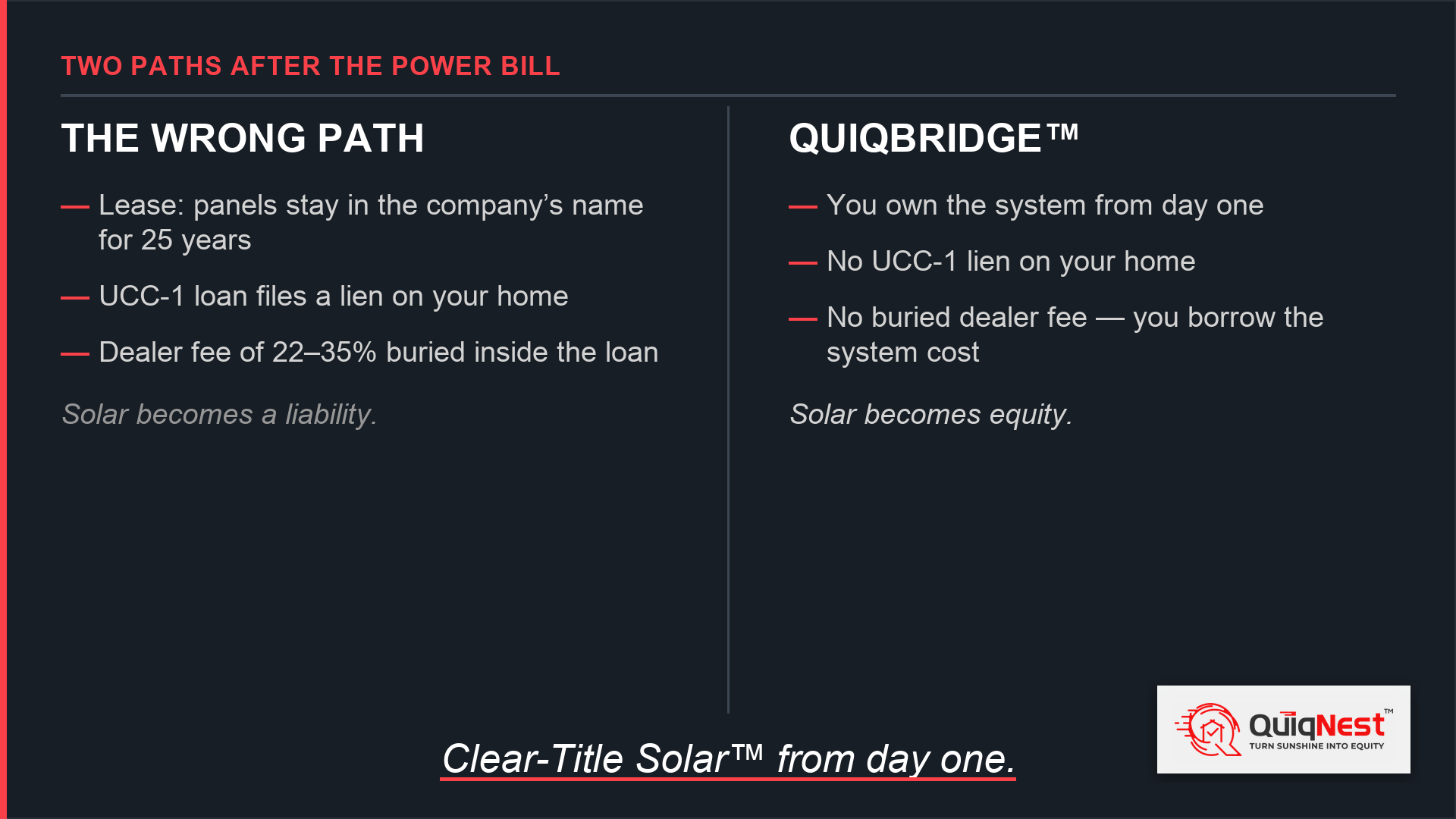

Most homeowners get pushed toward one of two paths.

A solar lease puts panels on the roof, but the system stays in the leasing company's name for a 20 to 25 year term. The homeowner does not own the asset. The home receives no contributory value for it on an appraisal.

A UCC-1 solar loan lets the homeowner buy the system, but the lender files a UCC-1 financing statement, which places a lien on the home. These loans also commonly embed a dealer fee of 22 to 35 percent inside the loan principal, with no line item disclosing it. A system that costs $25,000 becomes a financed balance closer to $33,750, and the homeowner pays interest on the full inflated amount for the life of the loan.

Both paths solve the power bill. Both paths create a new problem that surfaces later, at the title company, when the homeowner tries to refinance or sell.

The path that builds equity

QuiqBridge™ from QuiqNest exists to give recent homebuyers a third path.

With QuiqBridge™, the homeowner installs solar now and owns it from day one. There is no UCC-1 lien on the home. There is no buried dealer fee. The amount borrowed matches the cost of the system. The result is Clear-Title Solar™ from the moment the system is installed.

The structure is designed with the exit in mind. When the homeowner has built some equity or when rate conditions improve, the QuiqBridge™ solar is built to refinance cleanly into the primary mortgage through QuiqRefi™. The end state is owned solar, financed inside the mortgage, contributing to the home rather than encumbering it.

QuiqBridge™ is built for a specific homeowner. Someone who closed on a home in the last 3 to 12 months. Someone who does not have meaningful equity yet, so a cash-out refinance is not yet an option. Someone who got hit with the power bill and wants to do solar without making a 25-year mistake. It is available in Florida and Texas, for systems up to $25,000, with terms up to 20 years and no equity required to start.

It is not the right tool for everyone. If you have not bought a home yet, financing owned solar directly into the purchase mortgage is the cleaner path. If you closed years ago and have built significant equity, refinancing directly is the better route. If you already have leased or UCC-1 financed solar on your roof, QuiqBridge™ cannot undo that. We say this plainly, because the category only works when the match is honest.

The warning you did not get

Nobody at the closing table warned you about the power bill. That gap in the process is not going to close on its own.

What you can control is what happens next. The bill is the trigger. The financing path is the decision. One path turns solar into equity in the home you just bought. The other turns it into a lien you will be explaining to a title company years from now.

If you closed in the last 3 to 12 months and the power bill is the reason you are reading this, run the Power Flip on your home at QuiqNest.com and see what the QuiqBridge™ path looks like on your actual address.