Florida Statute 553.996 Explained

How Pre-Purchase Solar Integration Supports FHA Clear-Title Solar™

Pre-Purchase Solar Integration

Florida Statute 553.996, formally titled the Energy Performance-Based Voluntary Option, was created to solve a growing problem in residential real estate transactions. Energy features were increasingly affecting buyer decisions, lender review, and long-term ownership costs, yet there was no standardized way to evaluate energy performance early without disrupting appraisal, title, or closing.

The statute provides a framework for voluntary, informational energy evaluation during the real estate process. It allows energy and solar considerations to be reviewed before a purchase is finalized, without mandating improvements, changing property valuation, or forcing financing outcomes.

This distinction is critical. Florida Statute 553.996 is not about installing solar. It is about enabling early, structured evaluation so buyers, realtors, and lenders can make informed decisions without introducing transaction risk.

Why the Statute Exists

Historically, energy upgrades and solar were addressed too late in the transaction cycle. Buyers would discover energy limitations after contract. Lenders would raise questions near underwriting. Appraisers would receive last-minute information that created confusion about value. Title issues could arise when solar financing introduced additional liens.

Florida Statute 553.996 exists to prevent late-stage disruption.

By allowing energy performance data to be reviewed before closing, the statute supports clarity, consistency, and transparency across all parties involved in a real estate transaction.

**What Florida Statute 553.996 Allows

And What It Does Not**

The statute allows property owners, buyers, or their representatives to voluntarily obtain energy performance information for planning and evaluation purposes. This includes reviewing how a property may perform from an energy perspective and whether future improvements could be feasible.

Importantly, the statute does not mandate solar installation. It does not require lenders to approve financing. It does not alter appraisal standards. It does not change underwriting criteria. It does not create valuation guarantees.

The statute is strictly informational. It creates space for early evaluation without triggering transactional consequences.

Pre-Purchase Energy Evaluation in Practice

In modern transactions, many lenders prefer early visibility into energy considerations, especially when a buyer is exploring future efficiency improvements or solar integration. This early review supports structural planning, not approval decisions.

Pre-purchase energy evaluation allows the transaction to remain clean and predictable. Appraisal remains based on the home itself. Title remains unchanged. Installation, if pursued, occurs later under a defined structure.

This approach reduces surprises and avoids the common problems that occur when solar is introduced after closing without prior planning.

How Solar-Ready Home PLUS™ Aligns With the Statute

Solar-Ready Home PLUS™ is an informational assessment designed to align with the intent of Florida Statute 553.996.

It evaluates a property’s potential for future solar integration using existing property data and, when available, historical energy usage. It does not authorize installation. It does not approve financing. It does not change the home’s value.

Instead, it provides clarity early in the process, allowing buyers and realtors to understand feasibility before making commitments.

This is why Solar-Ready Home PLUS is often requested during early lender conversations as part of pre-purchase planning.

FHA Clear-Title Solar™ and Pre-Purchase Planning

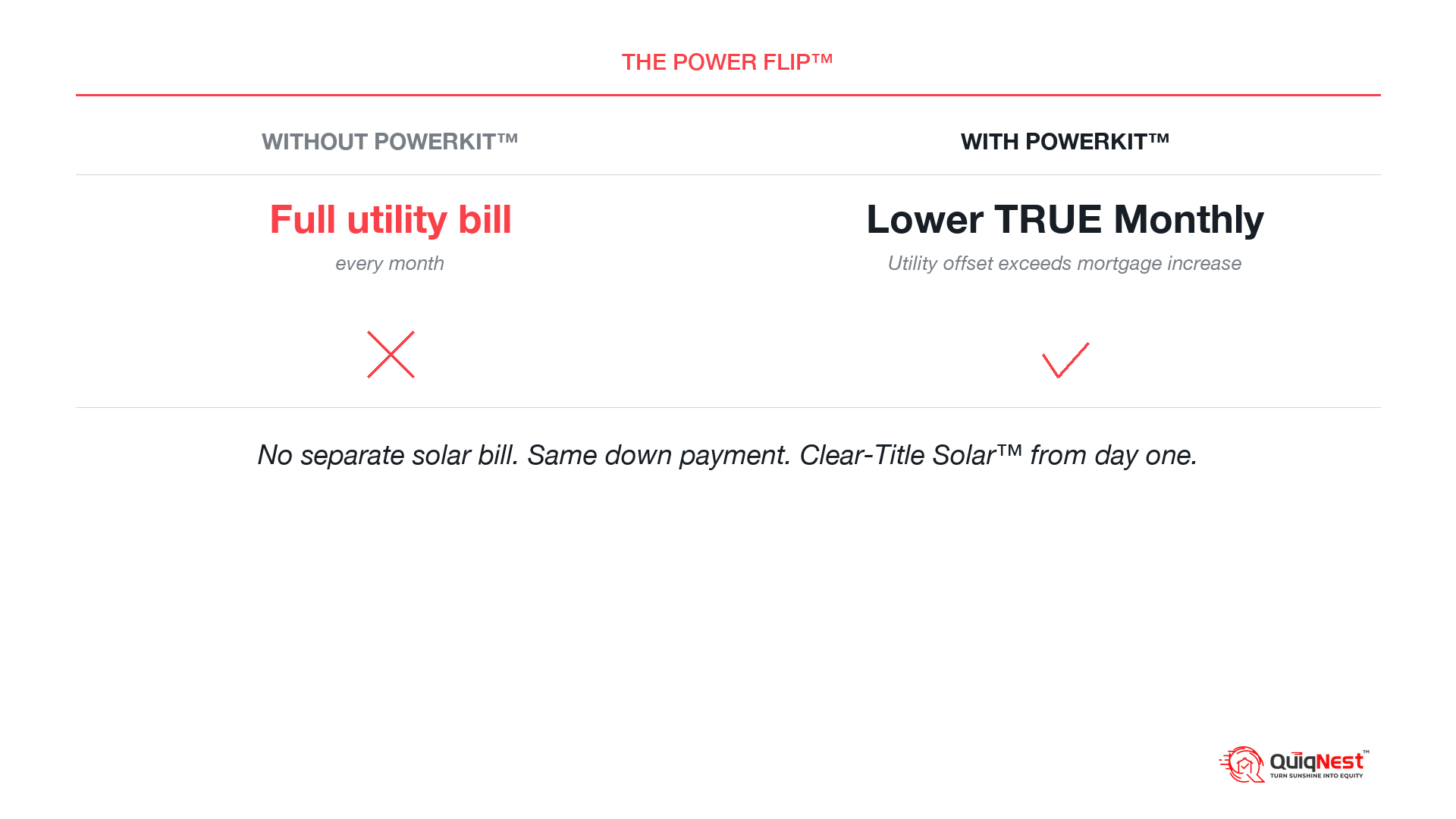

When a buyer later chooses to proceed, FHA Clear-Title Solar™ allows solar to be structured as a mortgage add-on, not a separate loan or third-party obligation.

In FHA Clear-Title Solar structures, the down payment applies to the home price only. No additional cash down is required specifically for the solar system. The solar portion is added on top of the primary mortgage as an energy-related add-on and installed after closing.

The home appraises on the home value alone. Title remains clean. No UCC-1 liens are created. Ownership remains singular and straightforward.

This structure is only possible when planning occurs early. Pre-purchase evaluation ensures solar is treated as an asset, not a liability introduced at the wrong stage of the transaction.

Why Early Evaluation Reduces Risk

Early energy and solar evaluation reduces appraisal confusion by separating planning from valuation. It reduces title risk by avoiding third-party encumbrances. It reduces closing delays by addressing questions before underwriting is complete.

Most importantly, it aligns buyers, realtors, and lenders around a shared understanding of what is being evaluated versus what is being installed.

That separation is the core principle behind Florida Statute 553.996 and the foundation of pre-purchase solar integration.

Closing Perspective

Florida Statute 553.996 provides the legal framework that allows energy planning to occur without disrupting real estate transactions. Solar-Ready Home PLUS operationalizes that framework. FHA Clear-Title Solar executes it cleanly when and if a buyer proceeds.

Together, they support a modern, lender-aligned approach to solar in real estate. One that prioritizes clarity, timing, and clean title.

Solar works best when it is planned early and executed correctly.

Educational Disclaimer

This content is provided for general educational purposes only and is not legal advice, financial advice, or tax advice. Real estate, lending, and energy considerations vary by transaction. Buyers, sellers, and professionals should consult appropriately licensed advisors regarding their specific circumstances.